Blake Lovewell

21st Century Wire

We will investigate the recent announcement of FedNow, a Federal Reserve instant payments service. We will elucidate what I see are the 7 key pillars that make up the CBDC system. In doing so we can watch how the process is unfolding with open eyes, and not be led astray into uninformed opinions. There is a global financial revolution occurring and we would do well to recognise it as it unfolds.

This article is a deep dive into CBDCs as they stand in Spring 2023, but also a launching off pad for deeper and more detailed researches on the topic.

On March the 10th of 2023 the United States Federal Reserve announced the new stage of its FedNow instant payments system. They intend to launch the system in July following a period of certification from April. Although originally announced in 2019, this latest decree has caused a real stir in alternative media and crypto space, with many critics expressing a growing concerns about an emergent banking system, one based on CBDCs – Central Bank Digital Currencies. In this article we will journey through the landscape of modern currency innovations to investigate how far along the road to a CBDC system we are and what it might look like. We will also evaluate the claims by both central bank proponents and opponents. Along the way I will attempt to define as many of the terms in use to make clear what is often an obscure subject for the regular citizen.

We might as well start with a broad definition of a CBDC. A Central Bank Digital Currency is a digital central bank liability. A central bank is a nominally private institution. It is usually not directly a facet of the government – though still a national institution – and it controls a nation’s currency. The decisions it makes can fundamentally change the lives of many millions, and transform the political economy literally overnight. They decide how much and when to print a currency as well as the rate at which the currency inflates or deflates by setting interest rates. The central bank for America is known as the Federal Reserve Bank, and it was inculcated on Jekyll island in 1910 by a shady group of financial elites. That however is a story for another time. What these central banks now propose in 2023 is a digital system, entirely based on computer networks, of liabilities and transfers. Liabilities by the way are simply debts or contracts – ‘I promise to pay the bearer of this note X or Y’. Originally these central bank liabilities were redeemable into real world assets like gold or silver, but steadily through the 20th century they found that they could slip out of this shackle. When Nixon decided to ‘temporarily pause’ the ability to convert dollars to gold in 1971, it signalled the end of the era of asset backed liabilities into the pure fiat system of today. A digital liability, a CBDC, would be a step further on this path; not backed by land, metal or any asset but simply backed by the word of an institution – ‘It is worth a Dollar because we say so’.

Moreover, a CBDC will shift control of the money supply away from the quasi-decentralised system we currently have, where money supply and ledgers are spread among region and national retail banks, and place the entire game into the hands of the central banks. This also raises serious questions about how governments and central bankers are going to keep Quantitative Easing (QE) and deficit spending thethered to reality (something they are struggling to do with the current fiat system).

Now we focus on the Federal Reserve initially as it is the biggest central bank in the world. Its currency, the US dollar was the global reserve currency – the money by which international trade was settled and the currency which for the last few decades oil was priced in. This was, as French ex-President Valéry Giscard d’Estaing dubbed it, America’s ‘exorbitant privilege’. Even as a multitude of factors have latently come to challenge the dollar’s hegemonic status, the Federal Reserve is still a prime mover in the central bank community.

As I researched the Federal Reserve’s activity on CBDCs I was led to FedNow’s resource page, I call it FedTown. It has the feeling of an attempt by the baby-boomer generation to make a slick, modern interactive webpage. One can navigate around the virtual town to dig into the mundane bureaucratic small print of the FedNow system. In passing I wonder how much was spent on this project. Yet determined not to be sidetracked I plowed through the paperwork to filter out some key points.

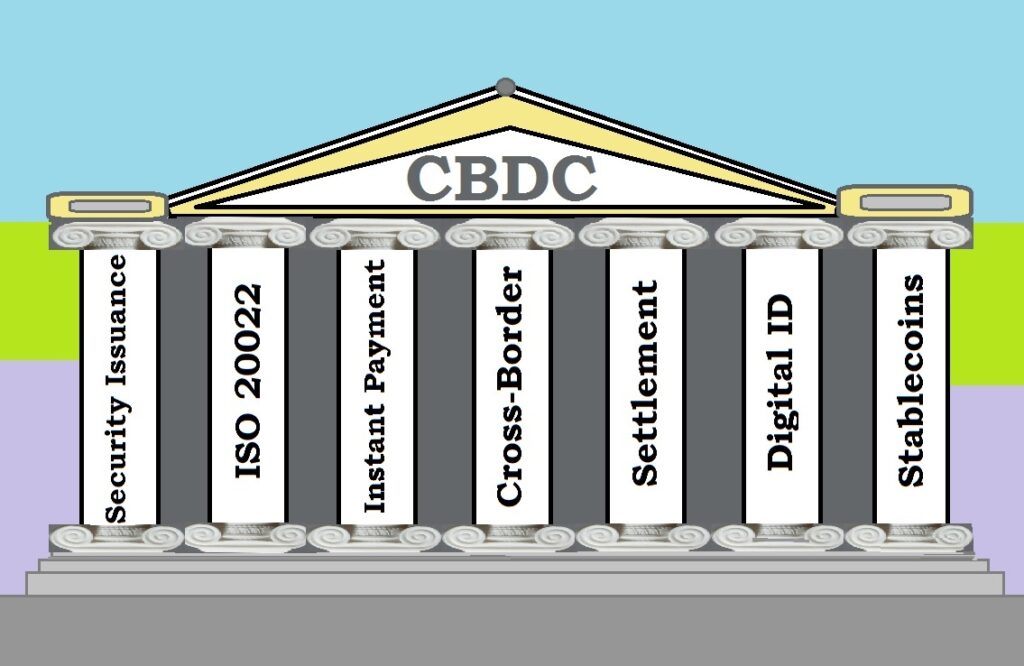

IMAGE: “The 7 Pillars” of Central Bank Digital Currency (CBDC).

The first pillar of a CBDC can be found in the ‘Faster Payments University Building’. Here we learn that the main purpose of the FedNow system is to provide ‘settlement’ of transactions both instantly and 24/7. In global parlance, this service is known as faster payment. “A “faster payment” is generally accepted to be “… a payment in which the transmission of the payment message and the availability of ‘final’ funds to the payee occur in real time or near-real time on or as near to a 24-hour and seven-day (24/7) basis as possible.”” Here they are quoting a 2016 working paper from the Bank of International Settlements, an important institution which we will address directly later. This quote reflects a global trend of a demand for instant settlement of transactions, not the usual 2-3 working days for a bank transfer to be finalised. It seems like an honourable cause and a means to bring the banking sector up to the 21st century. Yet it is only the most innocuous pillar of the CBDC that I will be discussing, and as such it will probably be the best advertised facet of the CBDC system.

To illuminate the next pillar we shall zoom over to ‘Technology Tower’. Here is the documentation which pertains to the implementation of the FedNow service for businesses and banks. It is here that I first heard about the second pillar of the CBDC system: ISO 20022. Now it looks like an eyesore, and promises to trip up most people trying to speak about the subject, but it turns out to be fundamental to global finance so it’s worth knowing about. The I.S.O. is the Geneva based International Organisation for Standardisation, borne out of the post-war globalising institution the League of Nations which later morphed into the United Nations. They make the standards for most everything in the world. You may see their acronym printed on fire alarm instructions, embossed on the sole of football boots or on an aircraft carrier’s exhaust pipe. As such they levy a lot of power, and as we are in the lift ascending technology tower I’ll give you a quick aside from Mark Shuttleworth.

““[ISO] is an engineering old boys club and these things are boring so you have to have a lot of passion … then suddenly you have an investment of a lot of money and lobbying and you get artificial results,”

Mark Shuttleworth (image, left) created Ubuntu, an open-sourced operating system. That means it is free to use and it is open in its creation, programming and updates. Unlike Microsoft, whom he has here critiqued, who used their influence to buy up the regulation process in the ISO to make sure that governments were locked into contracts to use only Microsoft’s operating system. That being said, we can presume the same critique holds true for generating regulation to do with international payments. Yet that claim would fall outside of the remit of this article, so as the lift doors open let us take in the full bird’s-eye view of ISO 20022.

Mark Shuttleworth (image, left) created Ubuntu, an open-sourced operating system. That means it is free to use and it is open in its creation, programming and updates. Unlike Microsoft, whom he has here critiqued, who used their influence to buy up the regulation process in the ISO to make sure that governments were locked into contracts to use only Microsoft’s operating system. That being said, we can presume the same critique holds true for generating regulation to do with international payments. Yet that claim would fall outside of the remit of this article, so as the lift doors open let us take in the full bird’s-eye view of ISO 20022.

In the words of the Federal Reserve: The financial services industry’s need for a common “language”” is what prompted the generation of ISO 20022. It is a messaging standard which is used in transactions to make sure that both parties are able to read the message clearly and without confusion. Messaging standards make it possible for varying institutions around the world to communicate. Uniquely, this language provides extra layers of data-rich communication, allowing lots of extra information to be bundled into a transaction. The Federal Reserve aren’t too open about what additional information might be included but they give us a hint in this quote: “Additionally, ISO 20022 messages provide the opportunity for enhanced analytics, which can lead to offering valuable new levels of payment services to financial institutions’ customers.” We will come back to this ‘enhanced analytics’ capability soon, but to précis it will involve lots of data about the user being transmitted in a transaction.

It is clear by now though that it is not just the Federal Reserve that has adopted ISO 20022 as their language of communication. In fact: “SWIFT estimates that 80% of global, high-value payments by volume will be processed through ISO 20022” by the year 2025. This regulation is being adopted rapidly, the world over. It is fast becoming the common language of global finance. To be involved in the global economy you will have to speak in ISO 20022 and to fail to do so, will leave you by the wayside. Now here is where the story gets interesting, for me at least, as ISO 20022 is also being imbued into certain cryptocurrencies.

Blockchain: A Global Ledger

As the Federal Reserve adopted the standard, some crypto investors highlighted the fact that Ripple (XRP) is also compliant. “[O]nly those digital currencies that are compliant with ISO 20022 may be used in a centralized setting. While many crypto enthusiasts note that cryptocurrencies are made to be decentralized, the progress global central banks are making on this front may be too enticing to ignore.” This is not an aberration. It is not easy to become ISO 20022 compliant, in fact you would need a team of experts putting in concerted effort to make a novel technology like a blockchain tie in with this global standard. This is the kind of work undertaken by INATBA, the International Association of Trusted Blockchain Applications, an agglomeration of crypto companies that tie in with mainstream finance. Not only do Cardano and Ripple fall under the INATBA banner but so do Barclays, a bailed-out UK based bank, the BNDES, the national investment bank of Brazil who are embroiled in huge scandal as well as the EU commission itself. Ripple too is in bed with the World Economic Forum. We are then facing a new form of ‘crypto’ which is a far cry from the decentralised dream that drove Bitcoin and the cypherpunk ideology which created cryptocurrency originally.

Now Ripple’s move into ISO 20022 is not just a sales pitch, it is a concerted effort to thrust their token, XRP, to the forefront of international finance. One of the key points of Ripple’s blockchain is On-Demand Liquidity. They provide a token whereby one can achieve nearly instant settlements by using their token as the middleman between transactions. This is not just a crypto bridge, it is a framework for global interoperability, the third pillar of CBDCs. The CBDC system is often touted as providing on-demand liquidity for real-time payments globally. Ripple is one to watch as this new global system rolls-out.

Ripple recently announced that it was partnering with Montenegro in creating a new CBDC for the country. This is big news as Montenegro currently uses the Euro. Therefore any innovation there must be signed off by the EU, and furthermore could signal a path forwards for the other eurozone members into the brave new financial world of CBDCs. This project is still in the development phase but we can find more real-world implementations of Ripple’s tech. They are involved in Singapore with their treasury’s CBDC-like product: FOMO Pay.

“Ripple, the leader in enterprise blockchain and crypto solutions, today announced a partnership with Singapore-based major payments institution FOMO Pay, which will utilize Ripple’s crypto-enabled enterprise technology to improve its cross-border treasury flows.” Here we find Ripple, tied in with the Singapore treasury for the purposes of central bank settlement. Settlement is the fourth pillar of a CBDC system, whereby central banks can transfer financial products like treasuries to each other. This is a way of distributing and marketising sovereign debt, those debts held by the nation or central bank. Currently this settlement process is laborious and political. Under a CBDC system it will be much easier for central banks to pass on their debts and will, in my opionion, lead to a more obscure system where the risk of debt-default is spread globally. Settlement has also usually been carried out under a national aegis, however here we have the transition to public-private partnership, which is a format which flows throughout the CBDC system.

Extending its tentacles further I found out that Ripple’s FOMO pay is at work across Africa and Asia and partners not only with Mastercard but also with China’s WeChat Pay. WeChat Pay is the financial arm of China’s everything-app WeChat where users can transact using a single login, the same as they use to socialise. Some commentators suppose that it could be a competitor for China’s e-Yuan, their CBDC. Yet WeChat Pay is already tightly regulated by the Chinese state, so there is already something of an overlap. I think that as we delve into the subject you might agree that these systems will soon become interoperable. I will highlight this with a quote:

“FOMO Pay was also one of the founding members of the Singapore Quick Response Code (SGQR) taskforce and contributed to the introduction of the SGQR – a national standard to unify all e-wallets and move towards promoting a cashless society in Singapore. FOMO Pay aims to build Asia’s first licensed gateway helping corporates connect with fiat and cryptocurrency.” – There we have it, FOMO pay is tied up with Singapore’s national government in an effort to unify e-wallets, the protocols that people transact with, and needless to say it is ISO 20022 compliant. This provision of wallets is sure to be a hot topic in years to come, for they who control the wallet, control the person. Furthermore FOMO pay are openly engaged in engineering a ‘cashless society’ something that was once touted as a conspiracy theory but which is now coming true.

Sweden, who are the most cashless European state, are experimenting with the e-Krona, “a digital component to cash” which is issued by the central bank – the Riksbank. The e-Krona is presented as a new digital form of cash but the truth is it is a CBDC. It won’t have many of the aspects of cash that we, the people, might appreciate: some measure of anonymity in use, no interference in transaction by third parties and a physical bank note or coin. The concept was announced in 2017, with practical experimentation taking place from 2020, so we can assume they are quite far along the path of having a practical CBDC ready to use. Of note in the process of this experimentation is the company R3 and their product, Corda.

![]() In the same network as the INATBA and Ripple is the product known as Corda created by a company called R3, a blockchain company, although they use the acronym DLT: Distributed Ledger Technology because it sounds cool. R3 use one of the technological innovations behind Bitcoin – the blockchain – to create new financial products. DLT or ‘the blockchain’ is a vital fundamental technology of a CBDC system that we must acknowledge, as all CBDCs use it in some way or another. A blockchain is simply a series of blocks of information whereby the publishing of each block verifies the previous blocks, and adds something new – imagine you are keeping a notebook but each new page contains a condensed form of everything up to that point. This helps avoid the loss of data, or the input of spurious data as the verification process runs throughout the blockchain. Cryptocurrency used this tool to ensure nobody could post a fake transaction and claim funds from someone’s wallet as it would have to be verified by every node in the network, a failsafe. However large corporation are using the novel technology to outsource lots of their time-consuming legal procedures. The biggest go-to for blockchain work is R3.

In the same network as the INATBA and Ripple is the product known as Corda created by a company called R3, a blockchain company, although they use the acronym DLT: Distributed Ledger Technology because it sounds cool. R3 use one of the technological innovations behind Bitcoin – the blockchain – to create new financial products. DLT or ‘the blockchain’ is a vital fundamental technology of a CBDC system that we must acknowledge, as all CBDCs use it in some way or another. A blockchain is simply a series of blocks of information whereby the publishing of each block verifies the previous blocks, and adds something new – imagine you are keeping a notebook but each new page contains a condensed form of everything up to that point. This helps avoid the loss of data, or the input of spurious data as the verification process runs throughout the blockchain. Cryptocurrency used this tool to ensure nobody could post a fake transaction and claim funds from someone’s wallet as it would have to be verified by every node in the network, a failsafe. However large corporation are using the novel technology to outsource lots of their time-consuming legal procedures. The biggest go-to for blockchain work is R3.

R3 work with the big boys and their product Corda is used by a veritable who’s-who of big money: HSBC, Morgan Stanley, Allianz, Goldman Sachs, ING, and the recently bailed-out Credit-Suisse. Corda allows these megabanks to leverage blockchain for a variety of purposes, it’s a one stop shop for mainstream finance to segue into de-fi, decentralised finance. They can swap assets between protocols, be they cryptocurrencies or central bank currencies. They can generate smart contracts which self-execute – eliminating costly lawyers. They can also use Atomic swap technology for instant transfer of assets without needing a middleman or bridging currency. In amongst their talk of streamlining workflows and expediting transactions comes a vital note for our discussion here: CBDC implementation.

R3 announced this year that they are working with the UAE’s central bank to create a CBDC. R3 alongside a company called G42 would provide the technology and infrastructure for the UAE to create a CBDC. The key points for the UAE’s issuance of a CBDC are bi-lateral CBDC trade with India -an interesting alliance, wholesale and retail CBDC – ie/ a digital currency for day to day use in UAE and finally, our fifth pillar of the CBDC system: international trade settlement. A global CBDC system will be in the benefit of global capitalism. As such it will provide a ‘frictionless’ method to settle international trade. A topic that often comes up in the discussions from big institutions is the ‘need’ for a CBDC as a solution to what they call ‘pain points’. These are those stopping blocks where one nation demands a fee for transacting in a different currency, or another nation invokes an import tax and some currency must be transacted across financial borders incurring a fee. Well in a CBDC system there is the possibility to seamlessly interact between, for example, the Reserve Bank of India and the UAE Central Bank, we posit perhaps that India could buy lots of oil from the UAE. There wouldn’t be those pesky regulations holding back the deal if it were to be executed by the leaders of both states under such a system and the money could be in UAE’s coffers by sundown.

In another case, R3 is conducting an experiment with the Banque de France, their central bank; alongside the Swiss Central Bank, the suspiciously re-vivified Credit-Suisse and the Bank for International Settlements. The experiment will be these institutions, I quote: “using wholesale CBDC to enhance speed, efficiency and transparency in cross-border settlement.” Settlement is one of the main jobs of big financial institutions and if certain big players are able to gain a stranglehold over that process, by the use of CBDCs, then they are well placed to control vast swathes of the global economy. I mentioned the Bank of International Settlements and it is worthwhile defining that they are the central bank for central banks. They operate at the center of the network of national central banks, pushing new policies and maintaining the status quo as it is today. Often times it is what they say that leads the way for all other central banks down the line, so they are one to watch. I note here that the BIS CBDC working group has announced a system of mCBDCs – multiple-CBDC bridging. Along with the central banks of each state, the BIS are working on a 4 way inter-operable system for trading CBDCs between China, Thailand, Hong Kong and the UAE.

Noting this international pressure from the BIS to create inter-operable CBDCs, I was interested to read that R3/Corda were tying in this system with cryptocurrency. Now I have mentioned how the cryptocurrency they intend to foster is far from the freedom-enhancing stuff of the 2010s. In fact this illuminating document, I would say, is a must read if this interests you too.

In it we find a neat description of almost all of the 7 pillars of the CBDC system: Issuing securities, digital ID, ISO 20022 compliance, instant payments, cross-border interoperability and settlement. But they also bring up the pillar which is, in my opinion, the least understood: Stablecoins.

Now we may have thought that with the collapse of Silicon Valley Bank in March 2023 that stablecoins were falling out of favour with institutional finance. Silicon Valley Bank held most of the dollar deposits which backed Circle, the corporation who mint USDC, the second biggest stablecoin. A stablecoin is a virtual version of a currency, in Circle’s case, the US Dollar. SVB hold in Circle’s account the correspondent amount of Dollars to back up the issuance of UDSC virtual dollars. It is noteworthy that the use of a privately created digital dollar is a structure that would be replicated by a US CBDC. One could posit that the targeted shutdown of certain US banks all related to cryptocurrency could fit an anti-crytpo agenda, as some have pointed out. Yet the FDIC actually stepped in to fund these banks’ shortcomings and bail them out. That means that Circle, who’s virtual dollar dipped to about 88 cents in March, have been re-floated and now are back to their Dollar peg. Circle are also a member of INATBA – and we assume are a part of the in-crowd for regulated cryptocurrency and blockchain products. This institutional backing leads me to the conclusion that Circle isn’t going away any time soon. But how does this fit in with the CBDC system? The answer could be illuminating – this IMF report suggests that privately created stablecoins could do the public facing role of interacting with customers and would be backed by the new form of money, the CBDC, a central bank liability. They call this synthetic CBDC (sCBDC):

“In the sCBDC model, which is a public-private partnership, central banks would focus on their core function: providing trust and efficiency. The private sector, as providers of stablecoins, would be left to satisfy the remaining steps under appropriate supervision and oversight”

Having this public-private partnership would protect central banks from anti-CBDC regulation, such as that proposed by congressman Tom Emmer. If the private sector did the issuance and management of the ‘stablecoin’ then the central bank would be firewalled from accusations of a centrally controlled currency. In US constitutional law the Federal Reserve is actually barred from hosting customer accounts, this sCBDC could be a workaround. As the IMF noted in their report, the world of fiat currency is in flux, and so we are still waiting for the dust to settle on this new form of banking.

As to the legislative process though; one point of note I found in Corda’s insightful report was the FDIC’s “policy sprint” on crypto-assets. To clarify: the FDIC is the Federal Deposit Insurance Corporation which was created after the Great Depression to back American banks in times of crisis. Now when it comes to making policy that affects millions of people and their life’s savings, I’m not sure that a ‘sprint’ is exactly what I would recommend. In this ‘sprint’ they are looking to apply the same framework of regulation to banking and ‘crypto-assets’. Note too that they use the term ‘crypto-asset’, never crypto-currency. They want to retain a monopoly on the definitions here so any crypto-currency you hold is simply an asset, just like a bond, a contract, a deed and so on, even if it has coin in the name and functions like money. A ‘sprint’ does not leave a lot of time for deliberation and we must be wary of what definitions get railroaded into law.

Deals Done in the Dark

Right now there is a lot of back room dealing around these definitions and whilst it seems nitty-gritty, the consequences of these definitions have massive ramifications. I must note that the SEC this week was forced to define its chairman, Gary Gensler’s, favourite stablecoin Algorand, as a security and thus not just a stablecoin. This means that the $1.6billion market cap stablecoin now has to be subjected to a much stricter regime of rules, plus it throws Gensler under the bus for shilling a profit-making enterprise whilst he was chair of the SEC. Perhaps this is one INATBA backed stablecoin that won’t be making it into the CBDC system. In all my digging into the FDIC’s policy sprint though I was once again reminded of the Swiss connection; “the FDIC will be engaging with the Basel Committee on Banking Supervision” to draw up their regulation.

It is not only the BIS, the ISO and the Basel Committee on Banking Supervision, all Swiss, that make up Europe’s financial innovation hub. We have mentioned too France, Montenegrgo and Sweden’s forays into the world of CBDCs. In fact the ISO 20022 standard was first used for the Single Euro Payments Area. Since the creation of the European Central bank 23 years ago over 5,000 European banks have shut down for good. Mario Draghi, president of the ECB for over a decade put the European policy of banking centralisation best when he said that there were “too many banks” in Europe. It can therefore be levied that there is an agenda in Europe to shut down retail banks. Now with the CBDC system we can see the new alternative coagulating.

I came across an interesting piece on Yahoo news reporting a speech which typifies the ideology of the European beuraucrat. It describes a speech by Belgian fiancé minister Mathieu Michel who coined the term ‘Europeum’ for his proposed blockchain. He was speaking at the announcement of an important piece of legislation for cryptocurrency, known as MiCA: the Market in Crypto Assets bill, a far reaching bundle of laws. He said: “The bloc now needs to develop its own blockchain that would be able to record property ownership, driving licenses and professional qualifications”. This is a step beyond just currency into personal information. To have a huge trove of information available on a state or EU blockchain would raise privacy concerns for many, yet that is not an uncommon proposition in this CBDC system. Although he may well be grandstanding, Michel’s speech highlights the fundamental tenet of CBDCs: data harvesting.

In fact the CBDC hinges upon this point, surveillance of the user, to function. This pillar of the CBDC system is one of the most troubling and is often the subject of hyperbole in alternative media. It can innocuously be titled Digital-ID, but the skeptics fear is not unfounded. In cryptocurrency many people have witnessed the expansion of KYC (Know Your Customer) legislation whereby crypto exchanges need a copy of your drivers license or passport, and a photo of you holding it, as well as a host of personal details simply to buy a fraction of a Bitcoin or other cryptocurrency. The CBDC system would actually take this much further. In its pursuit of “Identity Proofing” the Federal Reserve has detailed some of the means by which they will verify the identity of an account holder. Not only will they require identity documents and app-based verification such as facial photography, but they will also be assessing someone’s credit profile, public records held by the government, internal data and worryingly – online profiles. Yes the Federal Reserve will be checking your Twitter before you can pay for your groceries. This concept which we should hone in on though is what they call “alternative data” – data that comes from outside public records. Here they will use machine learning, those oft-touted AI robots, to trawl through the troves of data harvested from the world wide web to generate a picture of you, and use that picture to decide if you are valid for a Federal Reserve CBDC transaction. Looking forwards too, it is not only the Federal Reserve but private corporations such as JP Morgan who intend to use ‘biometrics based payments’ in the modernised financial future that is fast approaching. With iris scans, surveillance, and supercomputer analysis this system is starting to look more like a sci-fi dystopia.

So there we have it, the pillars of a CBDC system are already in place. There is the ability to easily issue securities and financial products on the blockchain, this process is streamlined with modern computer tools. There is the omnipresent ISO 20022 regulation which ensures that all modern banking technology is speaking the same language, and that any other is left behind. There is the much lauded instant payments service, the US’ FedNow, or Australia’s PIX service, which whilst offering nice quick transactions, comes at the cost of rigorous central bank control. We have the cross-border international, inter-operable nature of CBDCs too – truly a global system. Nations and corporations, cryptocurrencies and stablecoins can be traded across borders with little friction, as long as they play by the rules. There is concurrent international settlement too: the CBDC can grease the wheels of international trade, which will likely benefit the biggest players who can afford to buy into the regulated system. Enforcing the system we have the Orwellian system of digital ID, not only checking your bank details but your personal affairs and tying them into blockchains forever. And finally we have the panoply of surveillance tools, artificially supplemented to make sure that nothing escapes the CBDC system’s purview.

Conclusion

Undoubtedly, there is much to be wary of in the CBDC system. And there is so much more to be learned. We must avoid shallow takes and drive-by analysis on this issue, as many did upon the announcement of the FedNow’s roll-out. Some of those may lead to accusations of misinformation, as FedNow is not a CBDC, as many hallowed fact-checkers will line up to inform you. However, FedNow it is a vital and necessary pillar of the CBDC system – and that’s the key point. Nor is a Central Bank Digital Currency necessarily a bad thing (in an ideal, perfect world). However, looking at how the cards are falling, what with biometric IDs, AI surveillance, globalist synergy, UBI (Universal Basic Income), so-called ‘programmable money’, social credit and similar exclusionary tools and policies – there is a distinct flavour of centralised control now taking hold. It is an institutional inertia that should be resisted. The hub-bub around FedNow did not go un-noticed and the Federal Reserve have had to, in the last few days, issue a statement to clarify their intentions. “The FedNow Service is neither a form of currency nor a step toward eliminating any form of payment, including cash.” This shows that there is still a feedback between public opinion and private finance. In this great confidence game of global banking, they still need us to believe in their products, in their integrity, if they lose that then their house of cards topples. As long as we keep our finger on the pulse, and maintain level-headed and informed debate, then there is a path through the woods to an equitable future.

I do hope that you can take something beneficial away from this research and recognise some of its implications for your life, and potentially benefit by taking steps to protect yourself from the worst restrictions of the nascent global CBDC system.

***

READ MORE FINANCIAL NEWS AT: 21st Century Wire Financial Files

PLEASE HELP SUPPORT OUR INDEPENDENT MEDIA PLATFORM HERE