Shawn Helton

21st Century Wire

President-elect Donald Trump continues to fill key positions in the White House and in the process, there have already been some controversial cabinet selections.

This week the Trump transition team named former Goldman Sachs partner and ex-Soros Fund Management employee (turned Hollywood financier), Steve Mnuchin, as the US Treasury Secretary.

The Mnuchin pick, arrives simultaneously as long time billionaire pal of Trump, Wilbur Ross, former head of “Rothschild Inc’s bankruptcy advisory business,” becomes Commerce Secretary.

While Trump’s cabinet nominees for the White House have not yet been set in stone, the two selections mentioned above represent the type of financial syndicate we’ve seen in the Washington swamp for many years.

‘TOO BIG TO FAIL’ – (Photo Illustration Shawn Helton of 21WIRE)

The Financial Crisis & Goldman Sachs

In April of 2016, Mnuchin was tasked with being the finance chairman of Trump’s 2016 presidential campaign, paving the way for another Wall Street insider to head to the White House.

In early November, sources close to CNBC floated the idea that formerly scandal plagued JP Morgan Chase CEO Jamie Dimon, was also up for consideration for US Treasury Secretary before Mnuchin, a long time acquaintance of Trump was officially named.

The Mnuchin selection appears at odds with Trump’s anti-Wall Street campaign rhetoric, as well as his ‘drain the swamp’ mantra echoed towards the tail end of his presidential run.

In fact, the optics of Mnuchin’s appointment, seems to strike at the heart of the sub-prime mortgage-backed security lending which led to the 2007-2008 banking crisis.

During the economic crash, extremely high risk subprime mortgage-backed securities were crafted from bundled loans. A large amount of these types of mortgages were adjustable rate mortgages, where interests rates would be fixed for a certain number of years, eventually sky rocketing to astronomical increases, subsequently putting the burrower under water as the banks continued to sell these loans to investors. This was a critical aspect that led directly to the foreclosure crisis that swept across the nation in the aftermath of 2008.

According to an article featured in the money section of the website of How Stuff Works, we are reminded of the devastating effects of the 2007-2008 crash:

“In just the month of August 2008, one out of every 416 households in the United States had a new foreclosure filed against it [source: RealtyTrac]. When borrowers stopped making payments on their mortgages, MBSs [mortgage-backed security] began to perform poorly. The average collateralized debt obligation (CDO) lost about half of its value between 2006 and 2008 [source: This American Life]. And since the riskiest (and highest returning) CDOs were comprised of subprime mortgages, they became worthless after the nationwide increase in loan defaults began.”

Continuing, the article outlines how the hedge-fund Wall Street casino made a fortune by packaging mortgages into bonds to sell to investors:

“After MBSs hit the financial markets, they were reshaped into a wide variety of financial instruments with different amounts of risk. Interest-only derivatives divided the interest payments made on a mortgage among investors. If interest rates rise, the return is good. If rates fall and homeowners refinance, then the security loses value.”

In a bold and controversial move, the president-elect’s administration by way of Mnuchin, is looking to derail the Dodd-Frank Act, which was put in place in 2010 as a moderate buffer (if at all?) to restrict the type of bank lending that led to the most recent financial crash in 2008. However, naysayers of the ‘protective act’ say it’s much to soft on Wall Street, which is in need of tougher restrictions, as any new deregulation could be seen as an attempt to increase the coffers of larger investment banks.

In the passage below, The New American expands on this idea through revelations released by the NY Times:

“According to the text of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act, the law is supposed “to promote the financial stability of the United States by improving accountability and transparency in the financial system, to end ‘too big to fail,’ [and] to protect the American taxpayer by ending bailouts.”

However, as is usually the case with federal laws, Dodd-Frank does precisely the opposite. “In fact,” reports the New York Times’ Gretchen Morgenson:

Dodd-Frank actually widened the federal safety net for big institutions. Under that law, eight more giants were granted the right to tap the Federal Reserve for funding when the next crisis hits. At the same time, those eight may avoid Dodd-Frank measures that govern how we’re supposed to wind down institutions that get into trouble.”

‘MONEY MAN’ – Ex-partner of Goldman Sachs Steve Mnuchin nominated to head the US Treasury. (Image Source: mgtvwten.files.wordpress.com)

Although Mnuchin has cited that there’s a need to restructure the Dodd-Frank Act because it would bring economic growth to regional banks and potentially open lending up to smaller businesses – there is still a fear that this may be a revolving door for the central banks to profit from as well.

Zerohedge provides additional background details regarding Munchin’s career in banking:

“Some more on Mnuchin’s background: starting his career in the early 1980s as a trainee at Salomon Brothers before moving to Goldman Sachs in 1985, Mnuchin was front and center for the advent of instruments like collateralized debt obligations and credit default swaps. He has called securitization “an extremely positive development in terms of being able to finance different parts of the economy and different businesses efficiently.” The pitfalls of the financing method came later, he’s said.

Mnuchin’s father, Robert Mnuchin, was a partner at Goldman Sachs in the 1960s. The second-youngest of five siblings, Steven attended the prestigious Riverdale Country School and then Yale University, where his roommate was Edward Lampert, who would go on to become a hedge-fund manager and owner of Sears.”

“In addition to Goldman, Mnuchin also worked at Soros Fund Management, whose founder, George Soros, has funded many left-leaning causes. Where it gets even more bizarre is that Mnuchin has donated frequently to Democrats, including to Clinton and Barack Obama.”

“As a hedge fund manager, Mnuchin is part of a group of business people Trump has excoriated. In August, Trump said hedge fund managers were “getting away with murder” as he touted his proposal to end the so-called carried interest loophole, which gives private equity and hedge fund managers preferential tax treatment.

“The hedge fund guys didn’t build this country,” Trump said at the time on CBS’ Face the Nation. “These are guys that shift paper around and they get lucky,” he said. “They are energetic. They are very smart. But a lot of them—they are paper-pushers. They make a fortune. They pay no tax. It’s ridiculous.“

Trump’s disdain for Wall Street during his campaign run won’t soon be forgotten by his supporters as the president-elect’s antithetical banking rhetoric will only be magnified by bringing Mnuchin (along with his banking and hedge fund past) into the fold.

Mnuchin’s confirmation could be a contentious affair (if only for show) due to money made after his purchase of California’s IndyMac following the financial crisis. Bloomberg recently stated the following concerning Mnuchin’s role in the aftermath of the banking and housing meltdown:

“In 2009, during the depths of the financial crisis, Mnuchin joined with a group of former Goldman Sachs colleagues and billionaires to buy the remnants of IndyMac, which had collapsed after bingeing on reckless home loans during the frenzy of California’s subprime-mortgage boom. They changed the name to OneWest, turned it around and sold the bank for a big gain last year.”

Continuing, Bloomberg outlines how Mnuchin may have seized on a financial opportunity but stops short of condemning the US Treasury nominee:

“It’s unclear whether OneWest’s practices were worse than those of other banks during the financial crisis or how much blame Mnuchin deserves for problems at a financial institution that was troubled before he bought it.

Mnuchin declined to comment through a spokesman. But former OneWest Vice Chairman David Fawer said in a statement that the bank inherited loans from IndyMac with “extraordinarily high delinquency rates” and “worked tirelessly to modify thousands of loans to help homeowners through the financial crisis.” The bank has pointed to positive reviews of its foreclosure and loan-modification practices by the Obama Treasury Department, the Federal Deposit Insurance Corp. and the Office of the Comptroller of the Currency.”

Interestingly, The Nation reported that Mnuchin purchased the failing IndyMac with an agreement to be ‘reimbursed’ for costs associated to foreclosures that were financed by the company:

The Mnuchin group paid FDIC $1.5 billion for the bank, far less than the value of IndyMac’s assets. The FDIC was so desperate to unload IndyMac that Mnuchin and his colleagues were able to obtain, as part of the purchase deal, a so-called “shared loss” agreement from the FDIC which reimbursed these billionaires for much of their costs for foreclosing on people unlucky enough to have mortgages from IndyMac.

Within a year, the group that the Los Angeles Times called a “billionaires’ club of private financiers” had paid themselves dividends of $1.57 billion. In other words, the FDIC took much of the risk by subsidizing the bank’s troubled assets, while Mnuchin and his colleagues pocketed the profits.”

Prior to considering Mnuchin, Trump was said to have considered former CEO of BB&T John Allison, an apparently harsh critic of the Federal Reserve banking system. The following was reported by Business Insider on November 28th:

“Trump will meet with John Allison, the former CEO of the bank BB&T and of the libertarian think tank the Cato Institute. There have been reports that Allison is being considered for Treasury secretary. Trump’s has on the campaign trail questioned the future of the Federal Reserve’s political independence, but Allison takes that rhetoric a step further. While running the the Cato Institute, Allison wrote a paper in support of abolishing the Fed.”

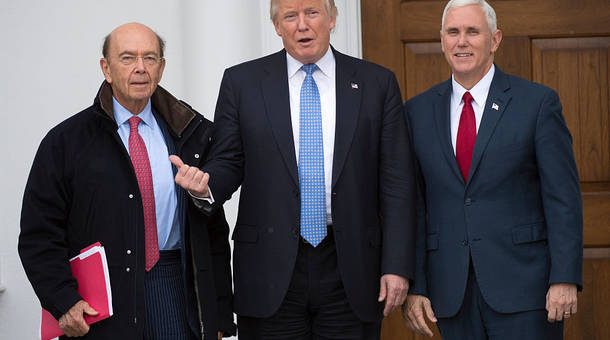

‘CABINET PICK’ – President-elect Donald Trump with fellow billionaire investor Wilbur Ross and vice-president-elect Mike Pence. (Image Source: (mediad.publicbroadcasting)

‘Insiders’ & The White House

Just as Mnuchin’s financial behaviour will be under watch, the same will hold true for the newly tapped Commerce Secretary position to be filled by billionaire investor Wilbur Ross.

A brief rundown of some of the more controversial aspects of Ross’s past were recently published at Forbes:

“After an getting an MBA from Harvard, he spent two decades heading Rothschild Inc’s bankruptcy advisory business, where he represented investors in Trump’s failing Taj Mahal casino in the early 1990s. Ross and Carl Icahn convinced bondholders to strike a deal with Trump, who some investors wanted to push out, which allowed Trump to retain control of the property.”

Continuing, the article described how Ross invested in distressed coal companies in addition to banking opportunities:

“During the recession Ross targeted another struggling industry: banking. He invested in troubled banks in England, Greece and Cyprus. He was also part of a group of investors that acquired a 35% stake in the Bank of Ireland during the height of Europe’s 2011 debt crisis. He sold the last of his stake in 2014, nearly tripling his initial investment. Ross has also reportedly bet hundreds of millions of dollars on downtrodden oil and gas firms since the price of oil began to slide more than two years ago.”

Incidentally, Ross has maintained a tough public position on so-called free trade deals like NAFTA and the soon-to-be defunct Trans Pacific Partnership (TPP) but real questions still remain about his financial acquisitions during distressed times – is he a risk taking business visionary or a financial vulture?

Ross has denied being a business liquidator for profit and states that he has worked to rebuild failing businesses.

Whatever the case may be, Mnuchin and Ross have touted big corporate tax relief and large tax cuts to the middle class in the US. However, the public should be wary of their dealings with those on Wall Street and any new reform legislation aimed at deregulation.

Banking deregulation and reform directed by Wall Street or one of their ilk, should be treated with great suspicion if history is any lesson…

Below is another look at a passage from a report I complied prior to the election entitled “PARTNERS IN CRIME: Goldman Sachs, The Clintons & Wall Street“:

“In one of the most significant financial rulings in the modern era, the Clinton presidency gave big banks like Goldman Sachs the skeleton key to the kingdom by deregulating the investment banking system almost entirely.

The Clinton/Goldman Sachs/Wall Street partnership was fully forged after the removal of the Glass-Steagall Act, which banking luminaries cynically named the “Financial Services Modernization Act of 1999” officially titled the Gramm-Leach-Bliley Act. The original Glass-Steagall was a depression-age four-part provision under the Bank Act of 1933 that strictly prohibited securities activities that could be harmful to investors – the same sort of rogue speculating and paper fiat fraud which triggered the Great Depression (1929-1941). In fact, the Gramm-Leach-Bliley Act which repealed Glass-Steagall, opened the door for the ‘shadow banking’ realm outside of regulatory oversight which led to a much higher trading risk, as banks became more interlinked.

Simply put: Clinton’s repeal of Glass-Steagell removed the firewall between speculative investment banking and regular high street retail and consumer banking – which exposed everyone to toxic, subprime ponzi schemes and fake paper products being pushed around the globe by the banking elite – which ultimately caused the global economy to crash in 2008. All that can be laid at the feet of one William Jefferson Clinton. And Hillary still claims that, “My husband did so well with the economy.” Really?

In a cross-posted article featured at Huffington Post, Nomi Prins underscored the complicit nature of Wall Street and Washington after the removal of tighter bank regulations under the Clinton administration during the 1990’s:

“To grasp the dangers that the Big Six banks (JPMorgan Chase, Citigroup, Bank of America, Wells Fargo, Goldman Sachs, and Morgan Stanley) presently pose to the financial stability of our nation and the world, you need to understand their history in Washington, starting with the Clinton years of the 1990s. Alliances established then (not exclusively with Democrats, since bankers are bipartisan by nature) enabled these firms to become as politically powerful as they are today and to exert that power over an unprecedented amount of capital. Rest assured of one thing: their past and present CEOs will prove as critical in backing a Hillary Clinton presidency as they were in enabling her husband’s years in office.”

Prins herself was a former managing director at Goldman Sachs, senior managing director at Bear Stearns, as well as having worked as a senior strategist at the now defunct investment banking firm Lehman Brothers. Following the financial crash in 2007-2008, Prins blew the whistle on the banking world in a book entitled “It Takes a Pillage: Behind the Bonuses, Bailouts, and Backroom Deals from Washington to Wall Street.”

Prins has become an advocate for the reinstatement of the Glass-Steagall Act since departing from the investment banking world.

The media outlet Common Dreams described the merger between Citicorp and Travelers Group (becoming Citigroup), which was dubbed the ‘Citi-Travelers Act’ on Capitol Hill. It was a conglomeration that went hand in hand with the Clinton administration’s influence on banking deregulation marked by the repeal of Glass-Steagall:

“Then, in 1998, in an act of corporate civil disobedience, Citicorp and Travelers Group announced they were merging. Such a combination of banking and insurance companies was illegal under the Bank Holding Company Act, but was excused due to a loophole that provided a two-year review period of proposed mergers. The merger was premised on the expectation that Glass-Steagall would be repealed. Citigroup’s co-chairs Sandy Weill and John Reed led a swarm of industry executives and lobbyists who trammeled the halls of Congress to make sure a deal was cut.”

At the time, it was the largest financial merger even though it was technically illegal, as stated by the former Bankers of America CEO Kenneth Guenther. In 1999, after “12 attempts in 25 years,” Congress passed the Financial Services Modernization Act, which led to the repeal of Glass-Steagall.”

Both of Trump’s finance picks arrive with the all to familiar baggage witnessed within the beltway swamp – and if Mnuchin’s and Ross’s questionable pasts are to be accepted wholesale, it’s difficult to imagine insiders of their pedigree turning over a new leaf for the “everyday man.”

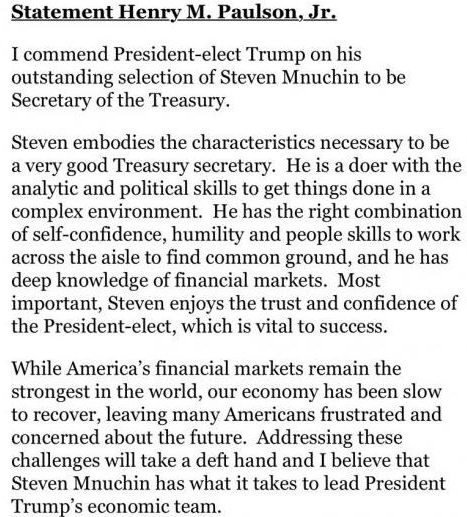

The following is a screen shot of a statement released by former Goldman CEO and former Treasury Secretary Hank Paulson regarding the Mnuchin pick. As a reminder, Paulson presided over the financial crisis and was US Treasury Secretary from 2006-2009. In 2008, amid a flurry of backlash, he authorized a $700 million dollar Troubled Asset Relief Program (TARP) banking bailout, masking the derivatives scam pulled by Wall Street’s top brass:

In 2010, CBS News cataloged the long relationship of Goldman Sachs and government, “revealing at least four dozen former employees, lobbyists or advisers at the highest reaches of power both in Washington and around the world.”

It’s also worth noting that White House adviser Steve Bannon and adviser Anthony Scaramucci have also worked for banking behemoth Goldman Sachs.

Will Washington see more Wall Street friendly policies under Trump?

READ MORE ELECTION NEWS AT: 21st Century Wire 2016 Files

SUPPORT 21WIRE – SUBSCRIBE & BECOME A MEMBER @21WIRE.TV

{kind=link}